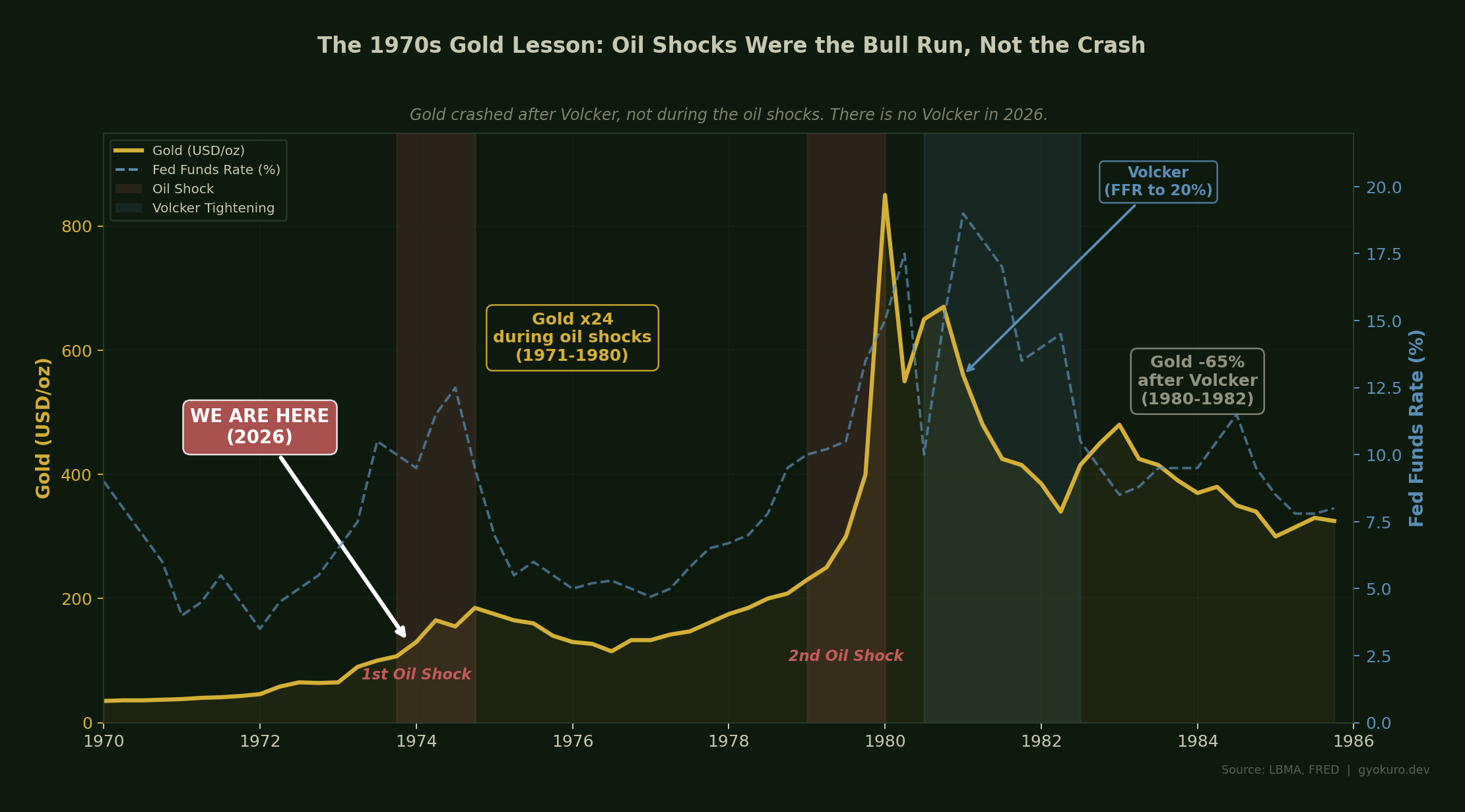

A fashionable argument is circulating in macro circles: the oil shock will kill gold. The logic runs as follows. Oil spikes. Inflation surges. The Fed tightens. Real interest rates rise. Gold, which yields nothing, becomes an expensive paperweight. QED. This is what happened in 1980, when Paul Volcker pushed the federal funds rate to 20% and gold crashed 65% from its January peak of $850.

The argument is clean, intuitive, and almost certainly wrong.

The precondition that does not exist

The 1980 gold crash had a precondition: a Federal Reserve chairman with the political mandate, institutional freedom, and sheer bloody-mindedness to impose a recession on the American economy in order to break inflation. Volcker had all three. He also had a public that, however grudgingly, accepted the trade-off. Inflation was running at 14%. The pain was visible, the cure identifiable, and the political system willing to absorb the cost.

None of those conditions hold today.

The Fed funds rate sits at 3.50-3.75%, unchanged since January. The FOMC is paralysed. Inflation remains above target but not at levels that demand emergency action. The oil shock is supply-driven, not demand-driven: hiking into it causes recession without fixing inflation, because American monetary policy cannot reopen the Strait of Hormuz. Markets are pricing roughly one 25bp cut for 2026, down from two at the start of the year. The Fed can neither tighten aggressively nor ease. It is frozen.

And the chair is about to change. Jerome Powell’s term expires on 15 May. Trump nominated Kevin Warsh on 30 January, but the Senate confirmation is blocked by Thom Tillis over the DOJ’s investigation into Powell. The judge quashed the grand jury subpoenas in March, calling the probe an effort to “harass and pressure Powell,” yet Tillis continues to hold. The FOMC meets this week. It could be one of Powell’s last meetings as chair, and the transition threatens to inject maximum uncertainty into an already febrile environment.

This is not a Volcker moment. This is the opposite of a Volcker moment.

The oil shock is gold-positive, not gold-negative

The people drawing the 1970s parallel are looking at the wrong half of the decade. Gold did not crash during the oil shocks. It surged. From 1971 to January 1980, gold rose from $35 to $850: a 24-fold increase. The crash came afterwards, when Volcker applied the cure. The oil shock was the disease, and the disease was extremely good for gold.

The current shock is, by the IEA’s own assessment, the largest supply disruption in the history of the global oil market. Brent crude closed above $103 on 14 March, having spiked as high as $120 earlier in the month. Tanker traffic through the Strait of Hormuz has effectively ceased. Gulf producers have cut at least 10 million barrels per day. The IEA’s unprecedented 400-million-barrel stockpile release has done nothing to reverse the trend. Iran’s new supreme leader has vowed to keep the strait closed.

Gold, meanwhile, is trading around $5,100. Up more than $2,100 from a year ago. Not exactly behaving like an asset that fears an oil shock.

The structural case is bipartisan

Strip away the geopolitics and the case for gold is simpler still: the dollar is being structurally debased, and no one in Washington intends to stop it.

The CBO projects a federal deficit of $1.9 trillion in FY2026, with debt held by the public at 101% of GDP and rising to 120% by 2036. Net interest payments alone are projected to consume over 20% of federal revenue. The deficit-to-GDP ratio is expected to average 6.1% over the next decade, more than double the Bessent target of 3%. The One Big Beautiful Bill has added roughly $2.4 trillion in unfunded liabilities over ten years.

Whether a Republican or Democratic administration occupied the White House, this trajectory would be identical. Both parties have demonstrated they will not cut entitlements, will not raise taxes to match spending, and will not accept the political cost of fiscal consolidation. The structural deficit is the structural case for gold.

The buyers who do not care about your yield curve

Central bank gold buying has become a structural constant. The PBoC has now purchased gold for 16 consecutive months, bringing reported holdings to around 2,308 tonnes, roughly 8% of China’s foreign exchange reserves. Estimated unreported purchases may be several multiples higher. J.P. Morgan projects central bank demand averaging 585 tonnes per quarter in 2026.

These are price-insensitive, strategically motivated buyers. They are not buying gold because they think yields will fall. They are buying gold because they are diversifying away from the dollar. The weaponisation of the dollar-based financial system after 2022 made gold the only reserve asset that cannot be frozen, sanctioned, or seized. This is a structural shift that operates independently of the Fed funds rate.

The scenario matrix

Three paths from here:

Contained resolution (perhaps 30% probability). The Hormuz situation resolves within weeks. Oil falls back towards $80. Inflation fades. The Fed eventually delivers one cut. Gold consolidates, perhaps pulling back 5-10% from current levels, but finds structural support from central bank buying and the fiscal backdrop. Floor around $4,500-4,700.

Stagflation muddle-through (perhaps 50%). Oil stays elevated. Inflation proves sticky. GDP growth, already revised down to 0.7% in Q4, weakens further. The Fed holds rates, unable to tighten or ease. The 10-year yield, currently around 4.27%, grinds higher on inflation expectations while the short end stays anchored. Real rates stay negative. Gold holds its bid and gradually moves higher. Target range: $5,000-5,500.

Financial crisis (perhaps 20%). The oil shock triggers a credit event. High-yield spreads, currently at 3.09%, widen sharply. The maturity wall bites. The Fed is forced to cut or restart QE to prevent a systemic crisis, regardless of inflation. Flight to safety. Gold surges. $6,000+.

In two of three scenarios, gold goes higher. In the third, it consolidates but does not crash. A crash requires a mechanism: someone willing to impose severe monetary tightening regardless of the consequences. The Fed cannot do this. Warsh, if confirmed, has signalled he favours lower rates. The political system will not tolerate a Volcker. The fiscal system cannot afford one.

The coming chairman shock

There is a further wrinkle. The Fed chair transition falls at the worst possible moment. Powell leaves on 15 May. If Warsh is confirmed, markets must price a new chairman’s reaction function into an active oil shock, an ongoing war, a fractured credit market, and an approaching maturity wall. If Warsh is not confirmed in time, the Fed enters the crisis without a permanent chair.

Either scenario is gold-positive. A new chairman cutting rates into an oil shock weakens the dollar and validates the structural debasement thesis. A leadership vacuum at the Fed during the largest supply disruption in history creates the kind of uncertainty that drives safe-haven flows. The gold bears need the Fed to behave like Volcker. They are about to get the opposite.

Gold at $5,100, with Brent at $103, the UST 10-year at 4.27%, the Fed frozen, the chair about to change, and central banks accumulating at record pace, is not overpriced. It is pricing exactly what you would expect in an environment of structural dollar debasement, geopolitical risk, and no credible inflation-fighting mechanism.

The 1970s parallel is instructive. But the lesson is not Volcker’s gold crash of 1980-82. The lesson is the ninefold run-up that preceded it. We are in the early innings of the oil shock, not the endgame. And there is no Volcker waiting in the wings.

The gold bears are importing a conclusion without its precondition.

– 玉露

This article is not investment advice. All data as of 14 March 2026 unless otherwise noted.