Part 1 was the demographic case. Part 2 was the regulatory and activist landscape. This is the spreadsheet.

Below book, almost everywhere

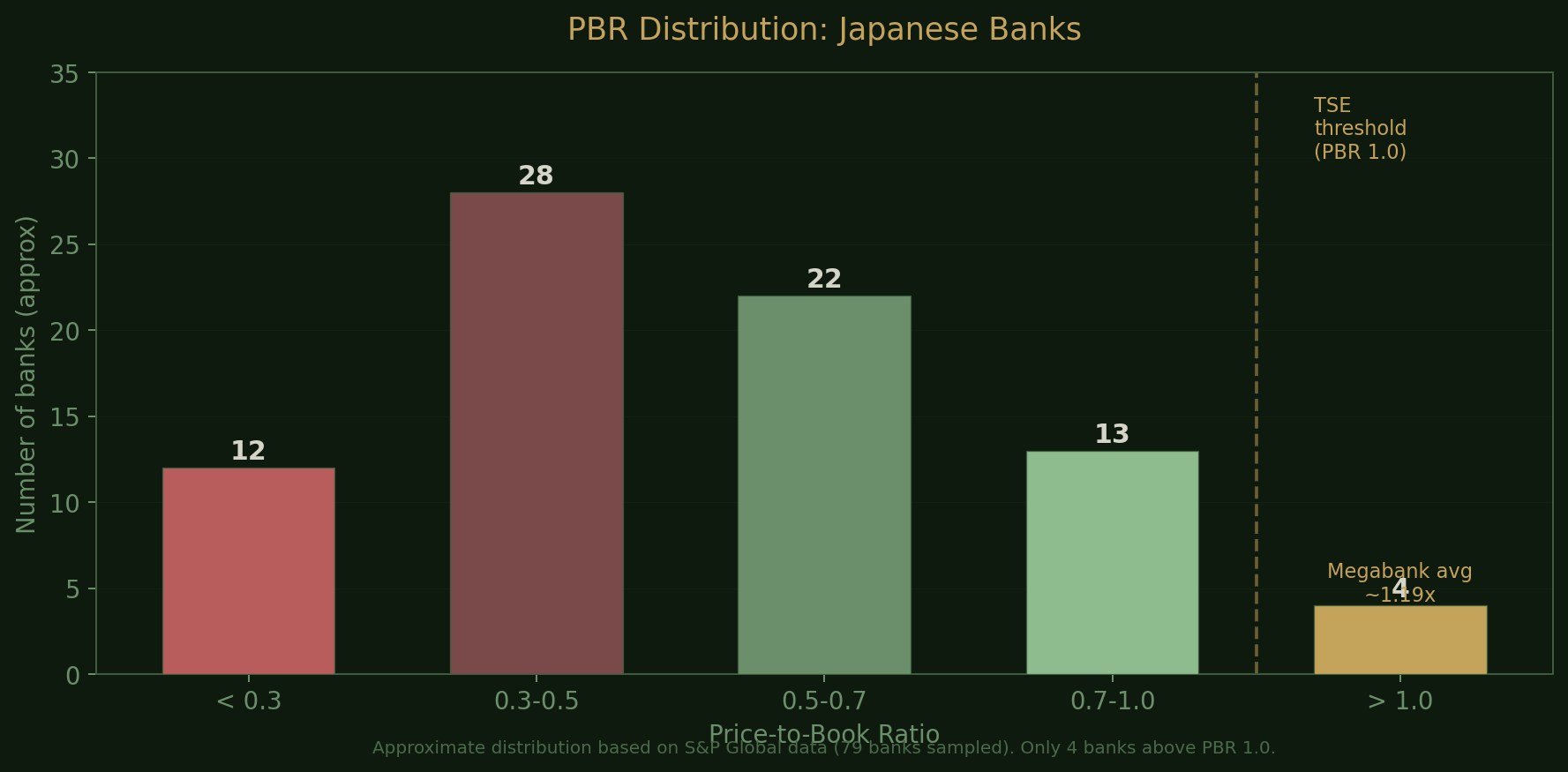

The Tokyo Stock Exchange’s 2023 directive to companies trading persistently below book value landed on the banking sector like an indictment. Of 79 Japanese banks surveyed by S&P Global, just four had a price-to-book ratio above 1. Half of all Topix stocks still trade below book value, the same proportion as twenty years ago, compared with 3% of the S&P 500.

The megabanks have since climbed to around 1.19 times book. Many regional banks have not. A significant number still trade well below 0.5 times book, with some under 0.3. A bank at 0.3 times book with 100 billion yen in net assets has a market capitalisation of 30 billion. The discount to stated asset value is 70 billion yen.

The TSE’s benchmark is clear: an 8% return on equity is considered necessary to justify a price-to-book ratio of 1. For most regional banks, getting there independently is arithmetically difficult when the revenue base is shrinking, non-interest income is negligible, and compliance costs are fixed.

The profitability divide

Not all 99 banks are equal. The dispersion of profitability across regional banks has widened over the past decade.

At the top sit institutions like Yokohama Financial Group and Fukuoka Financial Group, both with assets exceeding 20 trillion yen. They have diversified revenue streams, digital platforms, and the scale to absorb regulatory costs. Ariake Capital’s Tanaka has called 20 trillion yen the “threshold for survival”.

At the bottom are banks with a few trillion yen in assets, a single prefecture as their operating base, slowing deposit inflows, rising real estate exposure, and no independent path to digital transformation. The AML, cybersecurity, and system upgrade costs that regulators now demand are essentially fixed — a 5-trillion-yen bank and a 20-trillion-yen bank face much the same bill.

The FSA’s half-year results for regional banks through September 2025 showed aggregate net income up 26% year-on-year. But the growth was almost entirely driven by net interest income (+291.2 billion yen) and equity sale gains (+105.8 billion). Fee income grew by a negligible 2.3 billion. Bond losses deepened by 119.3 billion. The banks that cannot generate interest income gains — those with weaker pricing power and thinner loan books — are not participating in the headline improvement.

The acquirer’s arithmetic

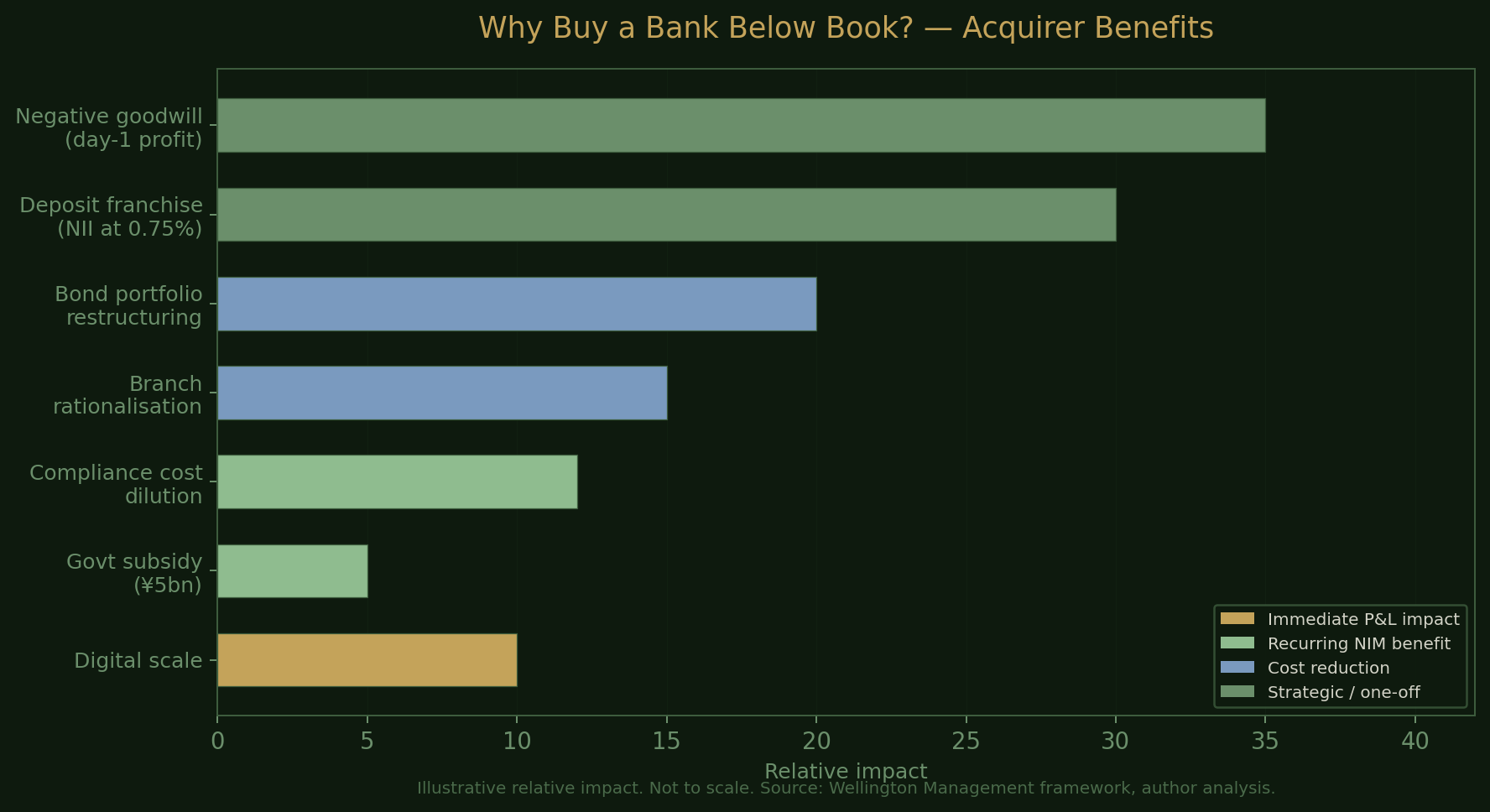

Here is where the narrative shifts. A bank trading at 0.3 times book is cheap, but cheap is not the same as attractive. What makes it attractive is what a buyer can do with it that the bank cannot do alone.

Wellington Management frames it precisely: acquirers benefit from “booking negative goodwill, restructuring low-yield bond portfolios, and boosting capital.” Targets trade at deep discounts “with improving fundamentals and untapped upside from interest-rate hikes and better capital management.”

The mechanics, unpacked:

Deposits have value again. Under negative rates, deposits were a liability with a cost. At a 0.75% policy rate, they are the raw material for net interest income. JRI’s Taniguchi notes that banks are now “eager to secure deposits potentially through M&A to earn higher margins.” Buying a deposit franchise below book value is buying earning assets at a discount to replacement cost.

Negative goodwill. Acquiring a bank below book value creates a day-one accounting gain equal to the discount. A bank purchased at 0.4 times book generates an immediate profit of 60% of the target’s net assets. This directly improves the acquirer’s reported ROE.

Bond portfolio restructuring. The target holds low-coupon JGBs it cannot afford to sell at a loss. The acquirer absorbs those losses against the negative goodwill gain, sells the underwater bonds, and reinvests at current yields. Net interest margin improves immediately on the acquired portfolio.

Branch rationalisation. Same-prefecture mergers allow consolidation of branches and ATMs, lowering overhead, while eliminating local competitors enhances pricing power. Two networks of 100 branches become one network of 140.

Compliance cost dilution. Regulatory and technology costs that are fixed in absolute terms become variable per unit of assets after a merger. The compliance burden halves overnight on a per-asset basis.

Government subsidies. The merger subsidy has been raised to 5 billion yen per deal, with a new system integration subsidy on top. The BOJ offers an extra 0.1% on current account deposits for banks that consolidate. The JFTC exemption eliminates competition review costs. The acquirer is being subsidised by the government, the central bank, and the regulator simultaneously.

The deadline. The JFTC’s antimonopoly exemption expires in 2030. Four years. Every deal that closes narrows the pool of available targets and raises the urgency for those still standing alone.

The rally that hasn’t happened yet

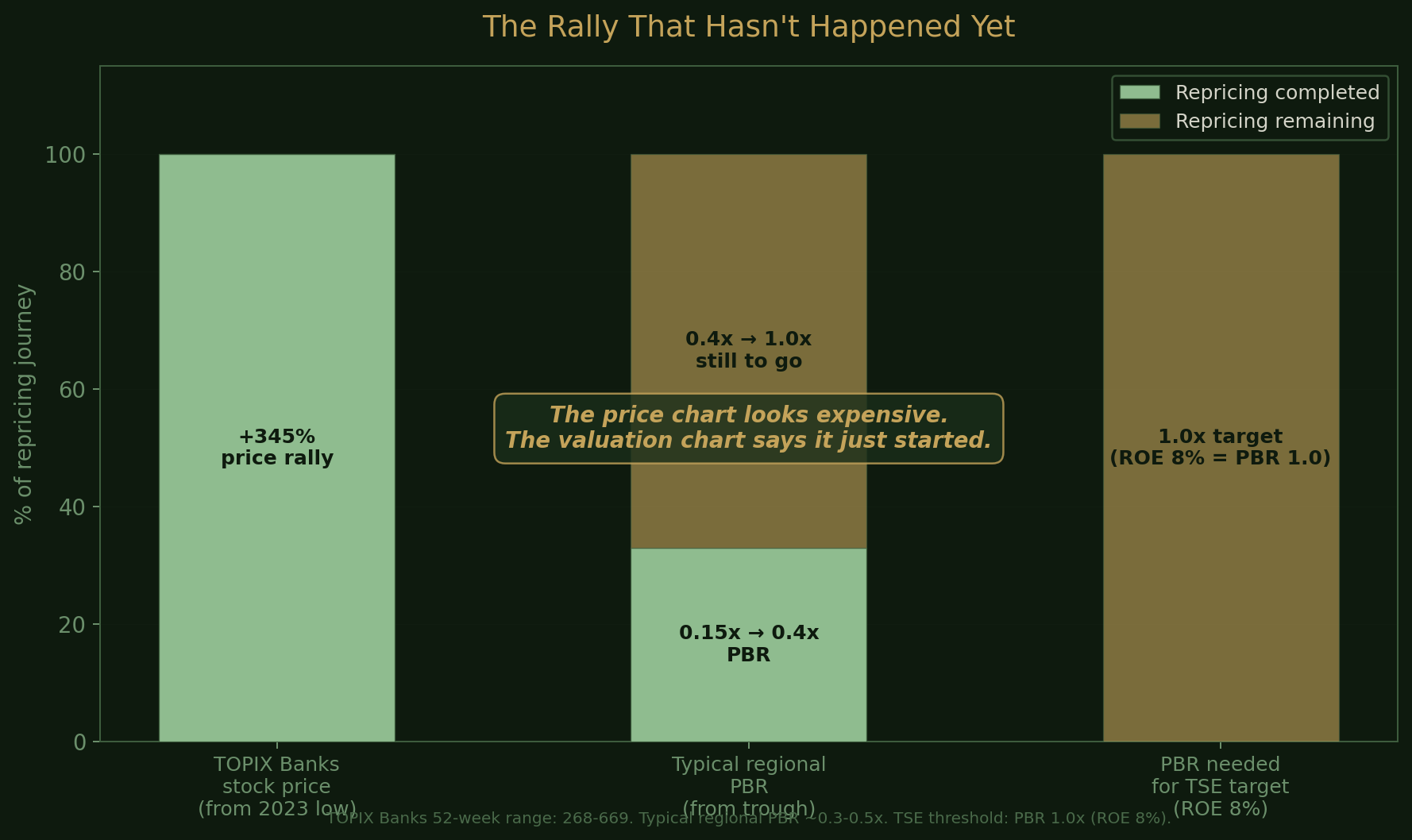

The most common objection to Japanese bank stocks is visual. Pull up a chart and the TOPIX Banks index has risen roughly 345% from its 2023 lows. The banks ETF returned about 41% in the past year alone. The instinct is: I missed it.

The instinct is wrong.

The stock price tripled. The price-to-book ratio went from approximately 0.15 to 0.4. The sector moved from “priced for bankruptcy” to “priced for managed decline.” It has not yet reached “priced for survival,” let alone “priced for consolidation upside.”

The TSE’s own benchmark says an 8% ROE justifies a PBR of 1.0. A typical regional bank sits at 0.3 to 0.5 times book. The arithmetic gap to 1.0 is a further 100 to 200% in share price appreciation — before any earnings growth.

And earnings growth is coming. The BOJ’s policy rate of 0.75% is a waypoint, not a destination. The estimated terminal rate sits between 1% and 2.5%. The NIM gamma described in an earlier article applies to regionals too, just with a longer transmission lag. Each additional hike hits an expanding loan book at a higher base rate. Interest income sensitivity accelerates.

Ariake Capital entered at these levels. SBI invested in nine banks at these levels. They are not buying because the stocks have rallied. They are buying because the post-consolidation value — negative goodwill gains, deposit franchise repricing, bond portfolio restructuring — sits multiples above the current share price. The market is pricing standalone decline. The activists are pricing integrated value. That repricing has not yet begun.

What the chart doesn’t show

The bearish case rests on the structural headwinds from Part 1. Population decline, deposit drain, real estate dependence. All correct. But several forces are working in the other direction, and most analysts are not discussing them.

Start with who is replacing the depositors. Japan employed 2.3 million foreign workers as of October 2024, up 12.4% year-on-year — a twelfth consecutive record. Manufacturing absorbs 26%, services 15.4%, and healthcare and welfare grew 28.1%. The government plans to admit a further 1.23 million under labour migration programmes by fiscal 2028. These workers concentrate in precisely the regional areas losing population — Nagasaki, Hokkaido, and Fukui are seeing some of the fastest increases in foreign residents. Every foreign worker needs a bank account. Japan’s population fell by 912,000 last year, but foreign residents grew by 354,000. The net decline is smaller than the headline, and the offset is concentrated in the regions.

Then consider the fee income that death itself generates. 912,000 deaths per year generate an enormous volume of estate settlements — account closures, inheritance verification, asset transfers. Regional banks, often serving as the deceased’s primary financial institution, process a significant share of these and collect fees on each. As household financial assets hit record highs, the average estate size is growing. The per-death revenue is rising even as depositors vanish. The demographic decline that erodes the deposit base generates fee income on the way out.

Government revenue is stickier than private deposits. Regional banks serve as designated financial institutions for prefectural and municipal governments — tax collection, pension distribution, public works payments, utility settlements. In ageing areas, per-capita government spending actually rises, because healthcare and social welfare costs are higher for an 80-year-old than for a 40-year-old. That spending flows through the local bank. Takaichi’s comprehensive economic package adds another layer: regional infrastructure, disaster prevention, national resilience, and defence are all rural spending categories. The fiscal expansion flows directly into regional bank lending pipelines.

Rural Japan also holds structural advantages in renewable energy. Wind, solar, and geothermal projects are disproportionately located in rural prefectures, and regional banks hold the local land relationships and permitting knowledge that megabanks lack. Project finance for a wind farm in Akita goes through the local bank, not through MUFG.

Two valuation anomalies compound the picture. Many regional banks still carry equity stakes in local companies at historical cost, with market values significantly higher. TSE reform is forcing eventual disposal, and the market has not fully priced the realisation of these gains — the banks look cheaper than they are. And after consolidation, the surviving entity controls 60 to 80% of a prefecture’s lending. The market is shrinking, but the bank IS the market. The Aomori Michinoku merger created exactly this: 80% market share in a prefecture losing 1.72% of its population annually. Pricing power in a declining pool is still pricing power.

Target characteristics

This article does not name targets. But the characteristics are identifiable.

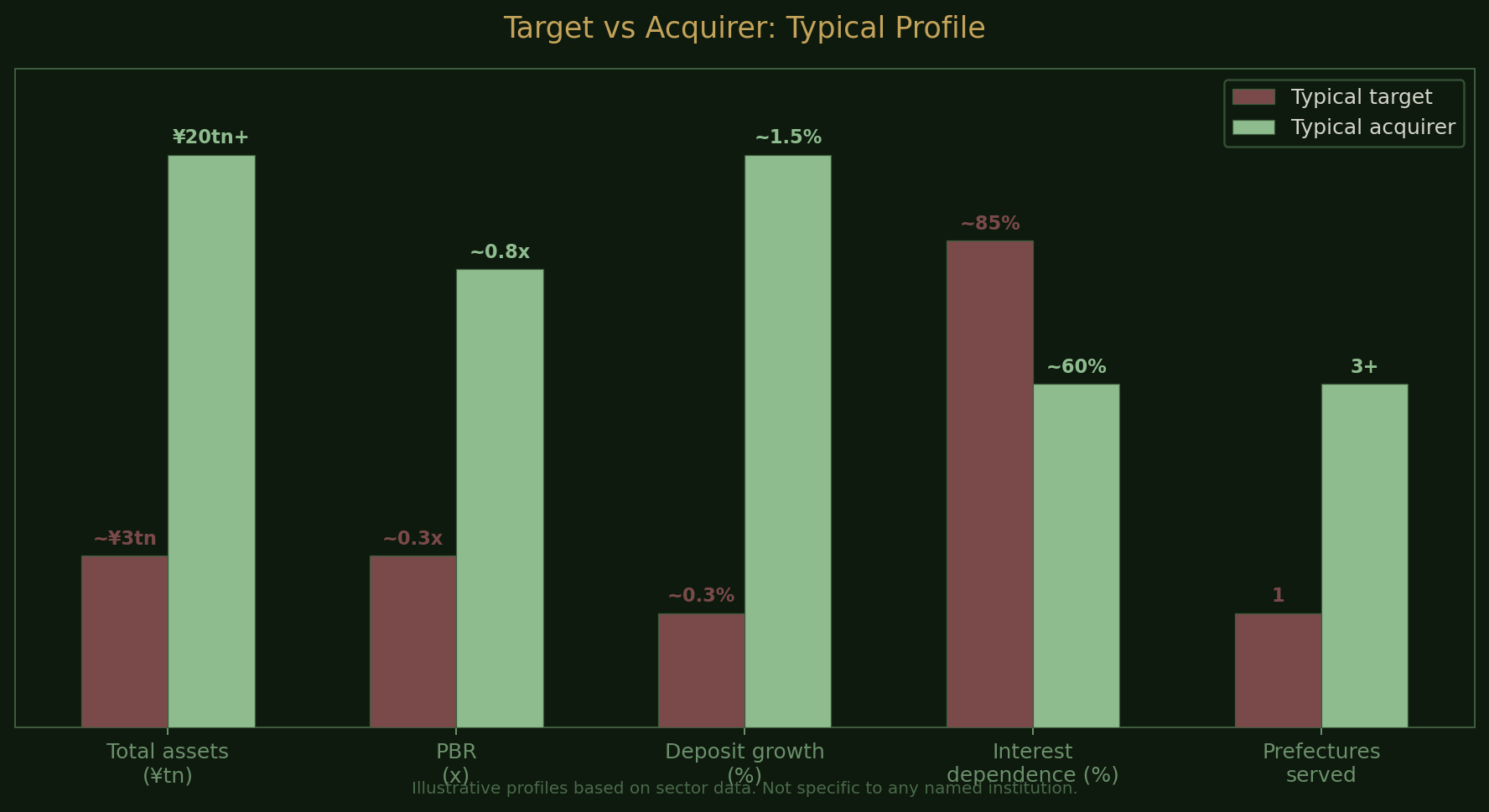

A bank likely to be acquired rather than to acquire tends to have: total assets well below the 20-trillion-yen survival line; a PBR under 0.5; operations confined to a single prefecture; a prefecture losing population at more than 1% annually; deposit growth below the already weak sector average of 0.9%; limited digital capability; and rising real estate concentration.

A bank likely to be an acquirer tends to have: assets above 20 trillion yen; a relatively higher PBR; a multi-prefecture or urban operating footprint; existing digital investment; and the capital headroom to absorb a target’s bond losses.

The old wiring is coming loose

Foreign investors examining this sector tend to focus on the numbers — PBR, NIM, population decline. They miss the invisible infrastructure that held regional banks in place for decades, and the fact that it is now dissolving.

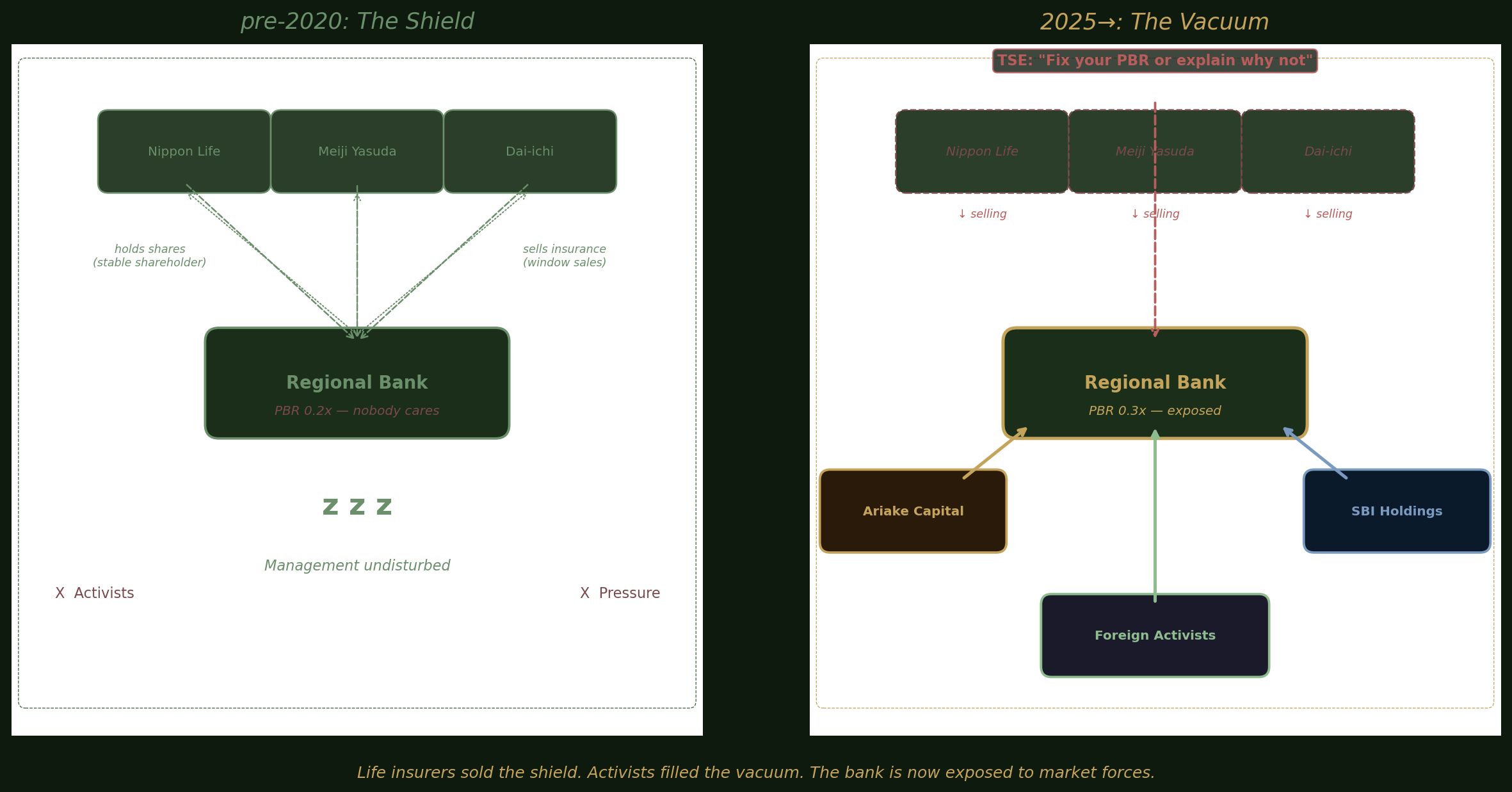

Japanese regional banks were long protected by a web of cross-shareholdings centred on life insurance companies. The mechanism was simple: a life insurer held regional bank shares as a “stable shareholder” (安定株主), and in return the bank sold insurance products through its branch windows. Nippon Life is a top-ten shareholder in 601 listed Japanese companies — roughly one in five of all listed firms. Meiji Yasuda Life belongs to the Mitsubishi corporate group, cementing ties to MUFG-affiliated regional banks. Dai-ichi Life maintains a comprehensive business alliance with Mizuho Financial Group.

What this meant in practice was that regional bank shareholder registers were filled with names that never complained. Life insurers collected dividends and window-sales commissions and left management alone. A bank could trade at 0.2 times book for a decade and face no shareholder pressure whatsoever. For entrenched management, this was the ultimate defence.

That defence is crumbling.

In 2021, Nippon Life announced plans to sell more than 20 billion yen in regional bank shares. Meiji Yasuda began its own reduction programme. Dai-ichi Life started notifying banks of planned disposals. Combined annual sales by major life insurers reached hundreds of billions of yen. The reason was straightforward: chronically low regional bank valuations were dragging down insurers’ portfolio returns. Separately, the megabanks joined in — MUFG, Mizuho, and SMFG announced combined cross-shareholding sales of $5.4 billion. The TSE’s PBR reform added regulatory urgency: 64% of TOPIX 500 companies still have more than 10% of net assets locked in strategic shareholdings, and the exchange wants that to change.

The sequence matters. When a life insurer sells its stake in a regional bank, the “friendly shareholder” disappears from the register. That creates a vacuum. Into that vacuum walk Ariake Capital, SBI Holdings, and foreign activists — investors who do not care about window-sales commissions and very much care about PBR.

The dissolution of the old keiretsu is not background context. It is the catalyst. The protective shield that allowed regional bank management to resist consolidation for decades is being withdrawn by its own holders. Every share sold by Nippon Life is a share that can be bought by someone with an opinion about what the bank should do next.

There is one more layer of hidden wiring that locals understand but outsiders rarely see: the core banking system.

Consolidation does not stop at prefectural borders. Fidea Bank merges Yamagata and Akita. Daishi Hokuetsu and Gunma Bank span Niigata and Gunma. The next wave will move by economic region, not administrative boundary.

There is another layer to read: capital ties.

SBI Holdings has invested in ten regional banks since 2022 (now nine after Chikuho Bank’s exit). It is negotiating with Shimizu Bank and Tsukuba Bank to raise stakes to 15% or higher, appoint executives, and introduce its proprietary cloud-based core banking system. Fukushima Bank and Shimane Bank have already adopted the platform. SBI Shinsei Bank, the alliance’s hub, has total assets of roughly 20 trillion yen, rising to more than 30 trillion including partner banks.

This is a modern keiretsu. Banks running the same core system face near-zero switching costs to full integration. The technology platform IS the capital relationship.

The table below is organised by regional cluster, with a column for known capital ties. This is not a recommendation list. It is a wiring diagram.

| Region | Prefecture (pop. decline) | Key banks | Status | Capital ties |

|---|---|---|---|---|

| Tohoku | Akita (-1.91%) | Akita Bank, Hokuto Bank | Hokuto+Shonai → Fidea Bank (Jan 2027) | |

| Aomori (-1.72%) | Aomori Michinoku Bank, Tohoku Bank | Merged (Jan 2025), 80% share | SBI → Tohoku Bank 3% | |

| Yamagata (-1.48%) | Yamagata Bank, Kirayaka Bank, Shonai Bank | Shonai → Fidea integration | ||

| Iwate (-1.69%) | Bank of Iwate, Tohoku Bank | — | SBI → Tohoku Bank 3% | |

| Fukushima (-1.37%) | Toho Bank, Fukushima Bank | — | SBI system adopted | |

| Miyagi (-0.51%) | 77 Bank | Tohoku’s largest; potential acquirer | ||

| Hokuriku-Koshinetsu | Niigata (-1.22%) | Daishi Hokuetsu FG, Taiko Bank | Daishi Hokuetsu + Gunma (target Apr 2027) | |

| Nagano (-1.05%) | Hachijuni Bank, Nagano Bank | Merged (Jan 2026) | 3-bank alliance (Shizuoka, Yamanashi) | |

| Fukui (-1.15%) | Fukui Bank, Fukuho Bank | Merger scheduled (May 2026) | ||

| Gunma (-0.84%) | Gunma Bank, Toho Bank | Integration agreed with Daishi Hokuetsu | ||

| Shizuoka (-0.55%) | Shizuoka Bank, Shimizu Bank | 3-bank alliance | SBI → Shimizu Bank 15% in negotiation | |

| Tokai | Aichi (-0.16%) | Aichi Financial Group, Bank of Nagoya | Ariake Capital 5.06% | |

| Mie (-0.80%) | Hyakugo Bank, San ju San FG | Toyota supply chain links to Aichi | ||

| Gifu (-0.93%) | Juroku FG, Ogaki Kyoritsu Bank | Extension of Aichi economic zone | ||

| Kansai | Osaka (+0.01%) | Kansai Mirai FG, Senshu Ikeda Holdings | Ariake Capital disclosed | |

| Shiga (-0.42%) | Shiga Bank | Ariake Capital disclosed | ||

| Wakayama (-1.42%) | Kiyo Bank | Sole bank in prefecture | ||

| Nara (-1.07%) | Nanto Bank | — | ||

| Kyoto (-0.50%) | Bank of Kyoto | Independent stance; strong franchise | ||

| Shikoku | Kochi (-1.71%) | Shikoku Bank, Bank of Kochi | — | — |

| Tokushima (-1.43%) | Awa Bank, Tokushima Taisho Bank | — | — | |

| Ehime (-1.19%) | Iyo Bank, Ehime Bank | — | — | |

| Kagawa (-0.82%) | Hyakujushi Bank, Kagawa Bank | — | — | |

| Kanto | Chiba (-0.13%) | Chiba Bank, Chiba Kogyo Bank | Chiba Bank acquired 20%, holdco forming | |

| Ibaraki (-0.77%) | Joyo Bank, Tsukuba Bank | Mebuki FG (Joyo + Ashikaga) | SBI → Tsukuba Bank 15% in negotiation | |

| Tochigi (-0.82%) | Ashikaga Bank | Mebuki FG | ||

| San’in | Shimane (-1.53%) | San’in Godo Bank, Shimane Bank | SBI system adopted | |

| Kyushu | Nagasaki (-1.39%) | Juhachi-Shinwa Bank, Nagasaki Bank | Juhachi+Shinwa merged | |

| Kagoshima (-1.12%) | Kagoshima Bank | Kyushu FG (with Higo Bank) | ||

| Kumamoto (-0.69%) | Higo Bank | Kyushu FG |

Notes: Population decline rates are 2024 estimates. Bank count includes Tier I and Tier II regional banks only. Capital ties based on Nikkei reporting (Dec 2025), regulatory filings, and company disclosures.

The table reads differently with capital ties visible.

Tohoku. Fidea crossed Akita-Yamagata. Aomori is done. But SBI holds 3% of Tohoku Bank, which operates across both Aomori and Iwate. Fukushima Bank is already on SBI’s core banking system. Miyagi’s 77 Bank is the largest in the region and outside SBI’s network. The acquirer in Tohoku is either 77 Bank, the SBI alliance, or both.

Hokuriku-Koshinetsu and Shizuoka. Niigata and Gunma are merging across prefectures. Nagano and Fukui are consolidating internally. In Shizuoka, however, two futures are emerging in the same prefecture: Shizuoka Bank (an independent large regional) sits alongside Shimizu Bank, where SBI is negotiating a 15% stake and system integration. One prefecture, two consolidation tracks.

Tokai. Ariake Capital holds 5.06% of Aichi Financial Group. Mie (Hyakugo Bank, San ju San Financial Group) and Gifu (Juroku Financial Group, Ogaki Kyoritsu Bank) are adjacent. Toyota’s supply chain runs across all three without regard for administrative borders. The auto parts makers borrowing from these banks operate in Aichi, Mie, and Gifu simultaneously. Ariake’s Aichi position reads as a bet on the entire Tokai economic zone.

Kansai. Ariake holds positions in Senshu Ikeda (Osaka) and Shiga Bank. Adjacent prefectures. Kyoto’s Bank of Kyoto has a strong independent franchise, but consolidation advancing around it narrows the room for standing alone.

Shikoku. Four prefectures, all declining 0.8 to 1.7% annually. Eight regional banks. Zero merger announcements. Zero disclosed activist positions. Zero SBI system adoptions. The largest blank space on the map. Blank spaces mean either that nobody has moved yet or that conditions are not ripe. The reader decides which.

The SBI map. Plot SBI’s positions: Tohoku Bank (Aomori/Iwate), Fukushima Bank, Shimizu Bank (Shizuoka), Tsukuba Bank (Ibaraki), Shimane Bank. They trace an arc outside the Pacific Belt, in the prefectures that megabanks ignore. Banks on the same core system already share integration infrastructure. SBI is building the plumbing before announcing the merger.

PBR data for each of these banks is available on Kabutan or individual bank investor relations pages. Place the names beside their price-to-book ratios, and the picture completes itself.

The reader who has followed this series from demographics through the merger window to these valuations has, by now, all the ingredients. What to cook with them is a personal decision.

This article reflects my own reading of publicly available information and is not investment advice.

— Gyokuro