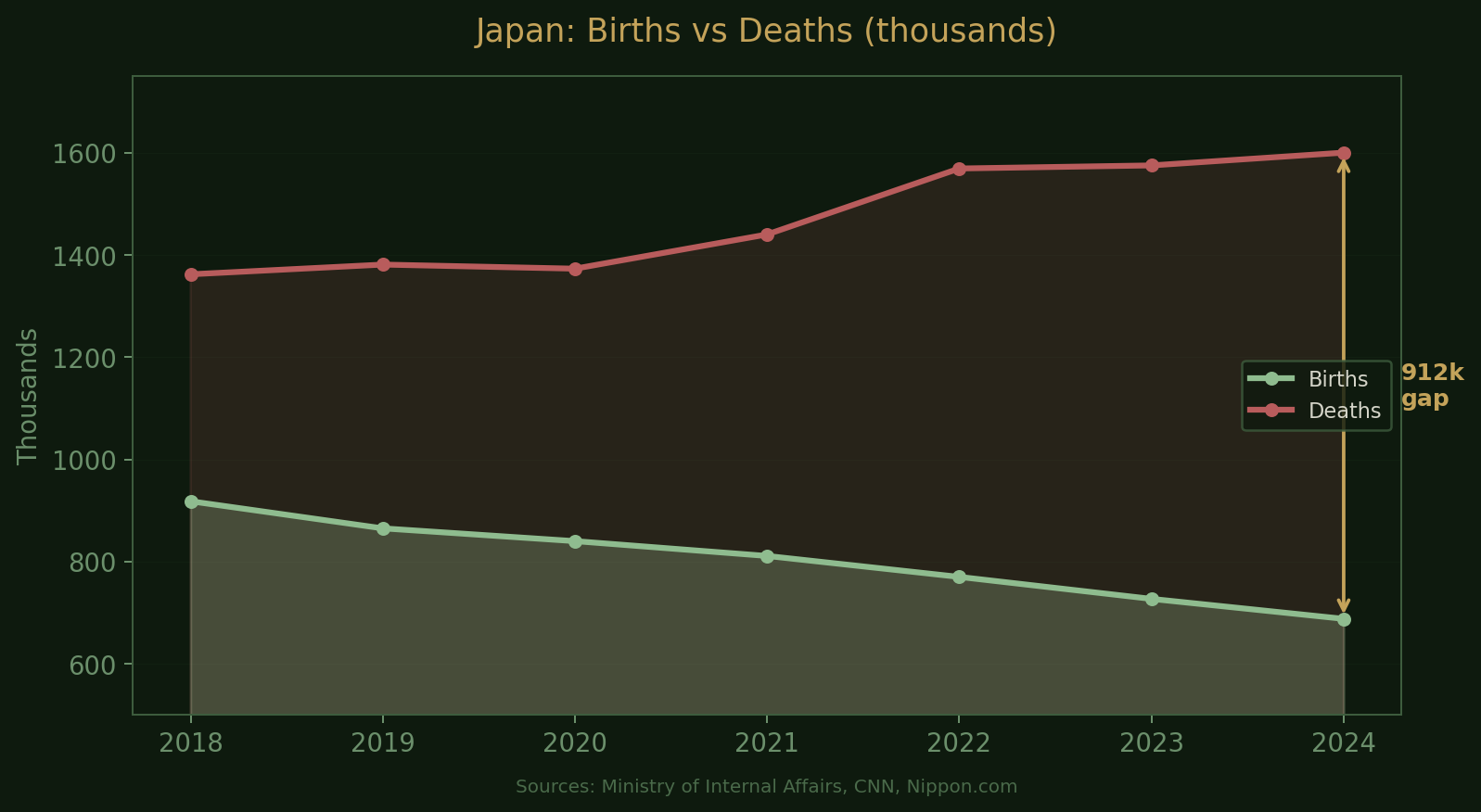

When an elderly woman dies in Akita Prefecture, her savings do not stay in Akita. Her children live in Tokyo or Sendai. The inheritance closes a regional bank account and opens one at MUFG, or flows into a NISA brokerage account, or both. Multiply this by 912,000 — last year’s record natural population decline — and you have the regional banking problem in a single transaction.

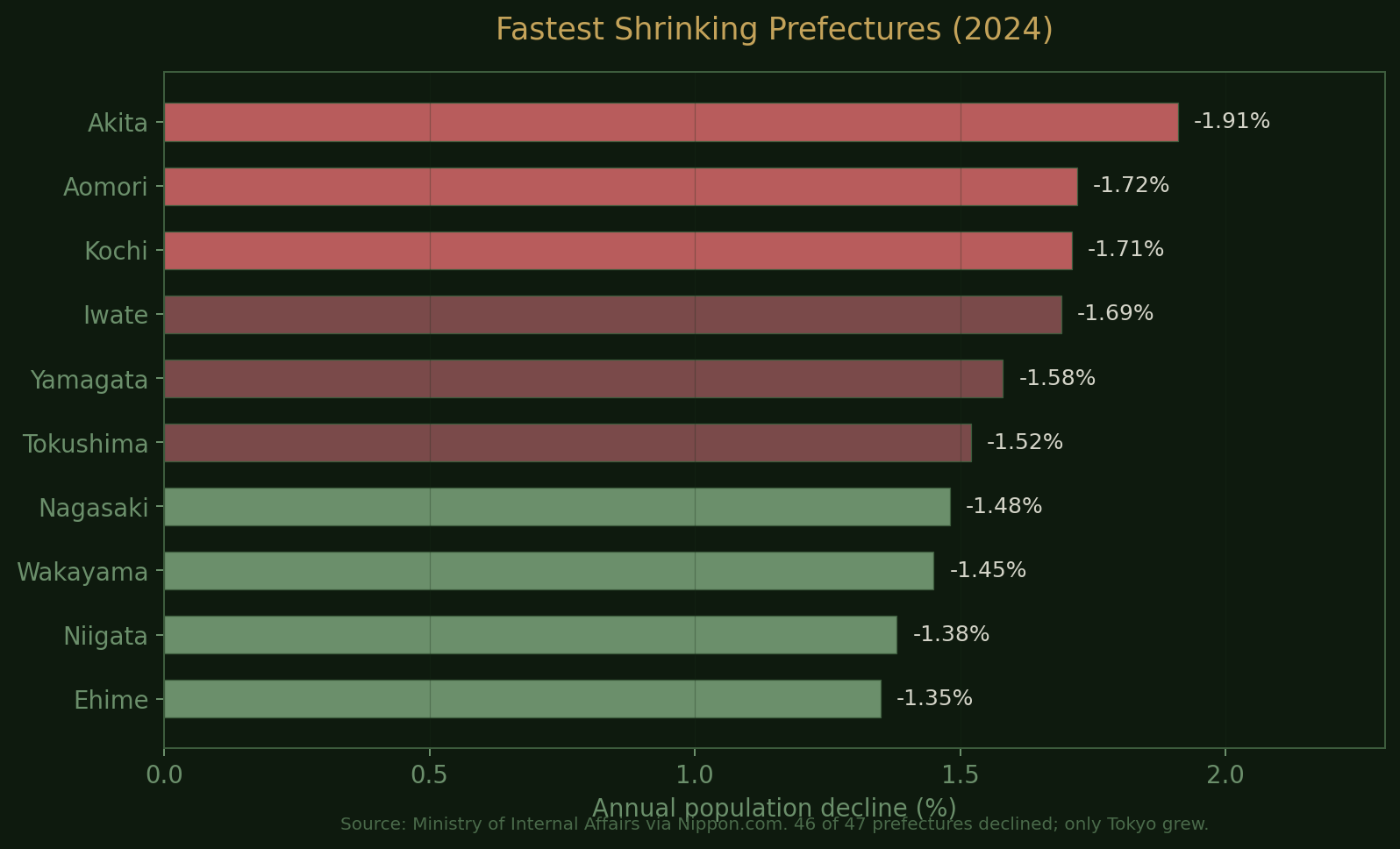

Japan has 99 listed regional banks. Sixty-two tier-one, thirty-seven tier-two. It has five city banks. The country’s population fell by 908,574 Japanese nationals in 2024, the largest annual decline since records began. Only Tokyo grew. All other 46 prefectures shrank. Akita lost 1.91%, Aomori 1.72%, Kochi 1.71%. In Akita, more than 40% of residents are already over 65. By 2050, its population is projected to be 60% of what it is today.

A regional bank’s business model is simple: gather local deposits, lend them locally. When both sides of that equation are contracting, simplicity becomes a problem.

The deposit drain

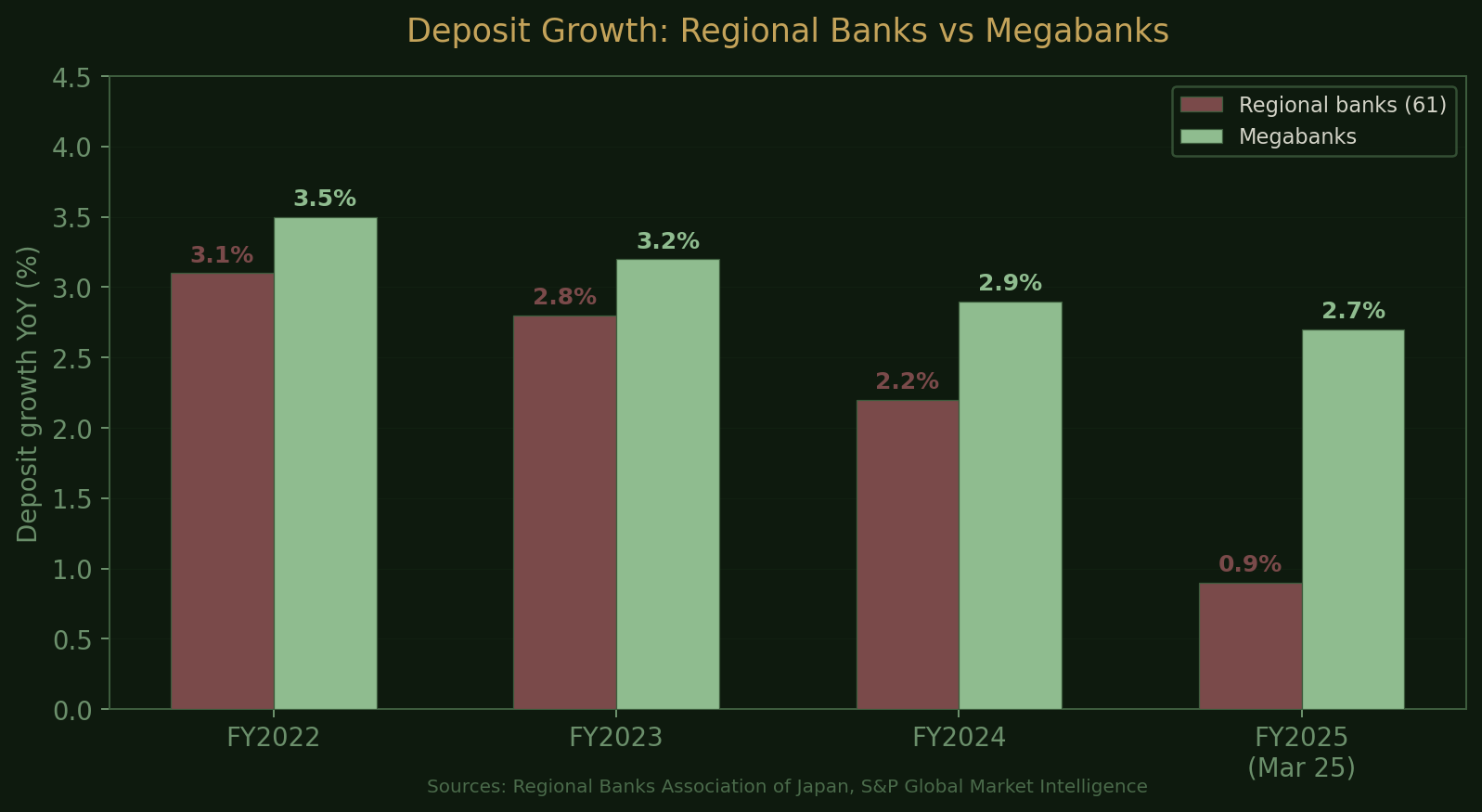

The numbers are plain. Combined deposits at Japan’s 61 main regional banks grew just 0.9% year-on-year as of March 2025, down sharply from 2.2% the year before.

Demographics alone do not explain the deceleration. NISA accounts have reached 27 million, siphoning younger savers out of bank deposits and into index funds — a nice irony, given that those index funds mostly buy foreign equities. Japanese retail money leaves the regional bank, leaves Japan, and buys Apple.

The loan-to-deposit gap fell to 108 trillion yen in December 2025, a four-year low. Loans per capita in regional areas are declining faster than deposits per capita, because borrowers — mostly small businesses — disappear along with the population that sustains them.

The competition for what remains is fierce. Megabanks, internet banks, and Japan Post Bank are all reaching into the same shrinking pool. Japan Post Bank alone operates 24,000 outlets, nearly double the combined branch count of all Japanese banks. Even so, its own deposits fell from 194.9 trillion yen to 192.1 trillion in the year to December 2024.

Not the megabank story

Readers of the previous article will recall the NIM gamma argument for megabanks: each rate hike compounds on an expanding loan book, producing accelerating profits. The regional story runs on different mechanics.

Regional banks cannot pass rate increases to borrowers as aggressively as megabanks can. Their clients are local SMEs that would struggle with higher rates. Deposit costs rise first. Lending margins follow slowly, if at all.

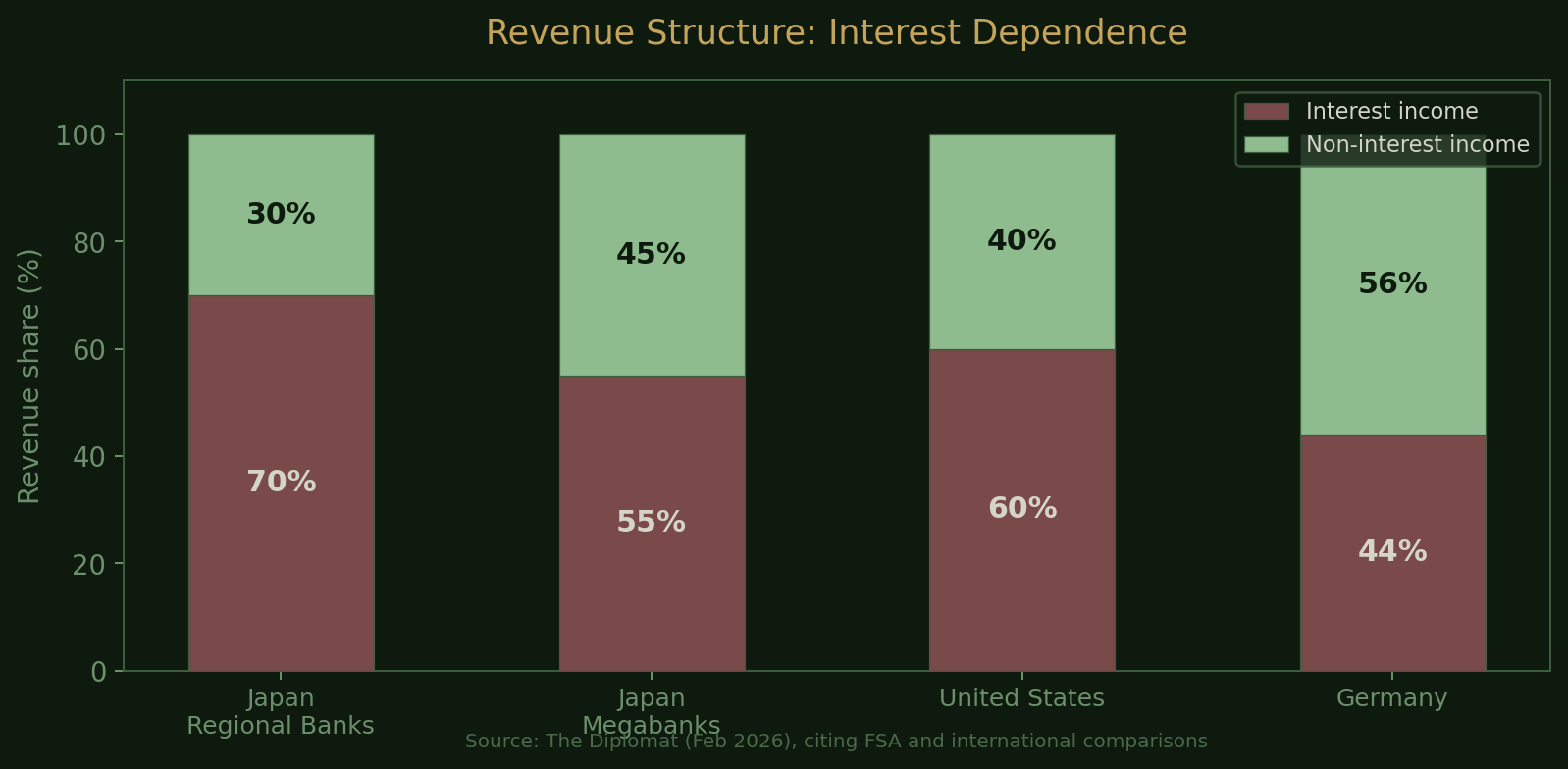

The structural gap is stark. Regional banks derive roughly 70% of their revenue from interest income. In the United States, the figure is 60%. In Germany, 44%.

The remaining 30% deserves scrutiny. The FSA’s half-year results summary for regional banks through September 2025 shows net fees and commissions grew by a mere 2.3 billion yen year-on-year. Investment trust distribution, ATM charges, transfer fees, insurance commissions — all essentially flat. These are commoditised, low-growth revenue lines with no structural tailwind.

Meanwhile, bond-related losses deepened to 248.2 billion yen, nearly double the 128.9 billion of the prior year, as rising yields forced regional banks to crystallise unrealised losses on their JGB portfolios.

What kept profits from collapsing was equity securities gains — 295.7 billion yen, up from 190 billion. This is cross-shareholding disposals, the same keiretsu unwinding that is flattering megabank earnings. The difference is that megabanks have other engines. For regional banks, once the holdings are sold, that income disappears.

Strip out equity gains and non-interest income is negative. The 70% interest dependence figure understates the problem. In practice, it is closer to 100%.

The FSA saw this coming. In 2018, it warned that more than 20 prefectures might not be able to sustain even one profitable regional bank. The population data since then has been worse than the forecasts.

The real estate crutch

Faced with a shrinking domestic loan book, regional banks have leaned into the one sector still generating demand: property.

Real estate loans account for approximately 17% of regional bank lending. Across all Japanese financial institutions, outstanding real estate loans reached 129 trillion yen at end-March 2024, up 6% year-on-year. Lending to special purpose companies for securitised property grew 18%.

The trouble is geography. Some regional banks have begun lending to real estate projects outside their home prefectures, chasing yields in Tokyo and Osaka that their local markets cannot offer. The FSA has noticed. In December 2025, it stepped up monitoring of regional banks with heavy property exposure, after identifying cases where repayment capacity had not been properly assessed.

On the mortgage side, megabanks are winning. Variable rates at the major lenders run 0.7-1.0%, slightly cheaper than regional competitors. Some regionals have responded by offering 50-year mortgage terms to attract younger borrowers. A bank that needs half a century to make a loan work is not operating from a position of strength.

The echoes of the 1990s are hard to miss. After the bubble collapsed, regional banks were weighed down by non-performing loans. They held about 185 trillion yen in assets at the time. Today they hold 500 trillion. The FSA is drawing the parallel itself.

The squeeze from both sides

Interest rate normalisation has lifted regional bank net interest income by 9% year-on-year as of September 2024. That sounds encouraging until you learn that the dispersion of profitability across regional banks is wider now than a decade ago. The strong are getting stronger. The weak are being pushed toward riskier lending or managed decline.

Both sides of the balance sheet are thinning. Population loss removes depositors and borrowers simultaneously. NISA removes the youngest and most digitally fluent depositors. Rising rates help margins but hurt bond portfolios — regional banks’ unrealised losses on yen bonds reached 3.3 trillion yen by September 2025, 2.6 times the level at the end of March 2024 when the BOJ first moved. The real estate lifeline, meanwhile, is attracting regulatory scrutiny.

Ninety-nine listed banks serving a country that loses 900,000 people a year. The arithmetic does not work. Something has to give, and in the next article, we will look at what is giving: the most significant wave of bank consolidation Japan has seen in thirty years.

This article reflects my own reading of publicly available information and is not investment advice.

— Gyokuro