Scott Bessent worked at Soros Fund Management across two stints between 1991 and 2015, doing one thing supremely well: spotting the moment when a central bank had mispriced risk and the speculative position on the other side was too large to unwind gracefully. When that moment came, the correction was violent. The people positioned for it made fortunes. Bessent was one of the best.

Now he runs the US Treasury. Japan holds roughly $1.2 trillion of American government debt, the largest foreign position — a mix of official reserves and private institutional holdings. If the yen weakens far enough, the private side of that equation starts to shift: life insurers and pension funds find hedging costs too high to justify holding US bonds, and new purchases dry up. US borrowing costs rise.

Bessent’s job is to keep Japan’s money flowing toward Washington. That means he needs the yen strong enough to make holding US debt attractive for Japanese investors, but not strengthening so fast that it detonates the carry trade and crashes global markets on the way.

The poacher became the gamekeeper. And right now, the poachers are reloading.

93,700 rounds in the chamber

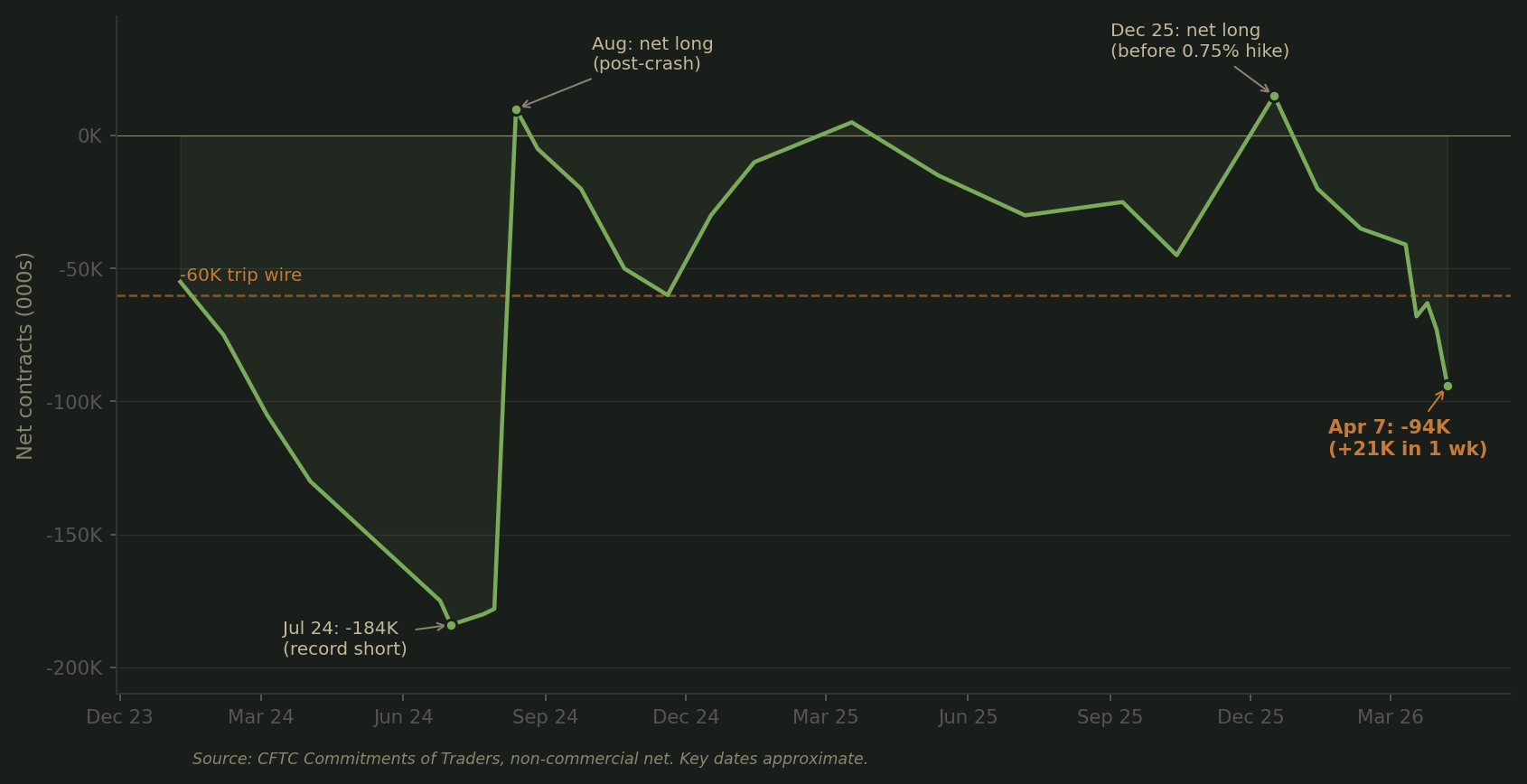

CFTC data from 7 April shows non-commercial speculators at −93,700 contracts net short the yen, up from −72,900 a week earlier. A jump of 20,000 contracts in a single week. Speculators are not preparing for a Bank of Japan (BOJ) rate hike. They are betting it will not happen. The next release, on 18 April covering positions as of 15 April, will show whether Ueda’s speech accelerated the buildup.

For context: in July 2024, yen shorts hit an all-time record. The BOJ hiked to 0.25% on 31 July and paired it with hawkish guidance. The Nikkei lost 12% on 5 August alone; speculators covered 46,000 contracts in a single week. The damage came not from the rate change but from the forced unwind of the position built around the assumption it would not happen.

In December 2025, the BOJ hiked to 0.75%. Nothing broke. CFTC was net long yen, OIS had priced the move at 98%. The market had already adjusted. No gap between positioning and probability, no explosion.

The lesson is not that BOJ hikes crash markets. The lesson is that the gap between what speculators are positioned for and what actually happens determines the violence of the adjustment. When the gap is narrow, the hike is absorbed. When it is wide, the hike detonates.

At −93,700 contracts, the gap is widening.

The man who blew out the match

On 13 April, Governor Ueda was in Washington for global policy meetings. His speech, read by Deputy Governor Himino in Tokyo, shifted the BOJ’s language. Previous statements had emphasised that rate hikes would proceed if the economic outlook was realised. The new speech dwelt on Middle East uncertainty and the need to monitor its effects on growth, inflation and financial stability.

The market moved immediately. OIS-implied hike probability for the 28 April meeting dropped from 60% late last week to roughly 33%. Former BOJ executive director Kazuo Momma called it “a close-call meeting” and said the BOJ’s instinct under uncertainty is to wait.

Speculators read the speech as permission. If the BOJ is hesitating, yen shorts are safe. Add more.

Bessent, attending the same Washington meetings, would have recognised the pattern immediately. He has seen this configuration before – from the other side of the trade. A cautious central bank statement lulls the market into complacency. Positions grow. The eventual correction, whenever it arrives, is larger than it needed to be. Ueda did not defuse the bomb. He gave the powder-stackers another week to work.

What Bessent actually wants

Bessent’s position on the yen is public and consistent. In January, Finance Minister Katayama said Bessent shared her concerns about the yen’s “one-sided depreciation.” In October 2025, he told reporters the yen would settle at a fair level if the BOJ follows a “proper policy path.” His Treasury readout from Tokyo last autumn urged the BOJ to communicate clearly and avoid excess volatility. When asked directly about US intervention, he said “absolutely not.” The message is clear: he wants the BOJ to raise rates. He does not want to do it for them.

But he does not want it to happen the way August 2024 happened. The ideal template is December 2025: the hike signalled well in advance, probability at 98%, shorts already covered, market absorbs the move without drama.

April 28 is shaping up as the opposite of that template. Probability at 33%. Shorts at −93,700. The gap wide and widening. If the BOJ hikes now, the man who spent his career profiting from exactly this kind of dislocation gets to watch it happen to his own balance sheet.

So what does Bessent actually want on 28 April? Almost certainly a hold – but with hawkish language that begins building probability for June. A hold validates the shorts in the short term. But if Ueda’s press conference signals that wages are strong, underlying inflation is on track and “conditions for the next adjustment are falling into place,” OIS for June starts climbing toward 60–70%. Some shorts begin to cover. By June, the position is smaller, the probability is higher and the hike lands without an explosion.

Signal first, price second, act third. The same playbook that made December painless.

Unless he has run the other calculation. Bessent’s toolkit is shrinking on a fixed calendar.

On tariffs, the Supreme Court struck down his use of IEEPA; the interim measures bridging the gap expire around July. On the Fed, Jerome Powell’s term as chair ends in May. Kevin Warsh’s confirmation hearing is set for 21 April, but Republican senator Thom Tillis is blocking the vote until a separate DOJ investigation into the Fed’s headquarters renovation is resolved. The Fed may enter the summer without a confirmed chair during a war. On Iran, the sanctions waiver is due for renewal.

Every month that passes, Bessent has fewer levers to manage a crisis.

If the carry trade squeeze is coming regardless – and at −93,700 contracts with the spread narrowing, it probably is – there is an argument that Bessent would prefer it now, while tools like a renewed eSLR exemption, Treasury buybacks, coordination with Japan’s finance ministry and verbal intervention could still be deployed. By July he could be fighting a carry unwind, a tariff cliff, an acting Fed chair and an expired sanctions waiver simultaneously.

Which calculation he has made is not visible in the public data. The weight of evidence – his call to Katayama from Davos in January urging her to “calm the market down,” the rate check when the New York Fed rang banks to ask about yen positioning, the October Treasury readout from Tokyo – points toward the December playbook as his preference. But preferences are not circumstances, and circumstances are deteriorating on a fixed schedule. The three numbers below will tell you which one prevailed.

Three forces Bessent does not control

Bessent does not control the BOJ. Three forces are pushing Ueda toward acting sooner than the market expects.

First, wages. The spring negotiations delivered above 5% for the third consecutive year. Real wages rose 1.9% year-on-year in February, the strongest gain in five years. The domestic inflation story the BOJ has been waiting for is arriving.

Second, the yen and the BOJ’s own numbers. At 158–159, import costs are rising. Household electricity bills jumped ¥15,000 from April. Petrol is at record highs. Economy minister Ryosei Akazawa said publicly that a stronger yen through rate hikes could ease this pressure. The BOJ agrees: Bloomberg reported on 14 April that the bank is considering a significant upward revision to its inflation outlook for fiscal 2026, driven by the oil shock, even as the growth forecast may be cut. The Outlook Report on 28 April will make this tension visible.

Third, board pressure. Hajime Takata has repeatedly dissented in favour of a hike, calling for a move to 1.0%. Takata is not a fringe voice. If Ueda holds in April and the yen weakens further, the dissent grows louder and the June hike becomes politically unavoidable – potentially at a moment when shorts have expanded even further.

The risk for Bessent is that the gradual approach he prefers is outwith his control. If Ueda judges that waiting creates more risk than acting, the hike comes into a market that was just told to relax. Markets are never more vulnerable than right after they have been reassured.

What to watch

The calendar for the next six weeks: 18 April CFTC release, 21 April Warsh hearing, 28 April BOJ decision and Outlook Report, May Powell’s departure, mid-May megabank earnings (next-year dividend guidance), July tariff bridge expiry.

If the 18 April CFTC data shows shorts expanding further toward −100,000, the system is more fragile than it was a week ago. If they have begun to cover, the market is starting to do Bessent’s work for him. The CFTC non-commercial net is free at cftc.gov; OIS hike probability is updated daily by Totan Research at tokyotanshi.co.jp/news.

The poacher’s dilemma

Once, Bessent would have been the one coiling the spring. He knows −93,700 contracts into a 33% hike probability when he sees it.

The BOJ meets in 14 days.