For three decades, betting on Japanese banks was an exercise in masochism. Negative rates crushed margins. Balance sheets swelled but profits did not. Then the Bank of Japan started hiking, and the masochists discovered they had been sitting on a convex payoff all along.

The three megabanks are on course for record profits. MUFG has guided for 2.1 trillion yen, SMFG for 1.5 trillion, Mizuho for 1.13 trillion. The common explanation is that higher rates mean fatter margins. This is true as far as it goes, which is not very far.

Not a straight line

SMFG’s investor presentation contains a number worth dwelling on: each 25 basis point rise in the policy rate adds roughly 100 billion yen a year to net interest income. That figure is not shrinking with each successive hike. It is a constant increment, but one applied to an expanding loan book. MUFG’s domestic corporate lending rose to 26.8 trillion yen; SMFG’s jumped 22% to 26.6 trillion. Rate times volume. The delta is getting bigger. In options parlance, NIM has positive gamma.

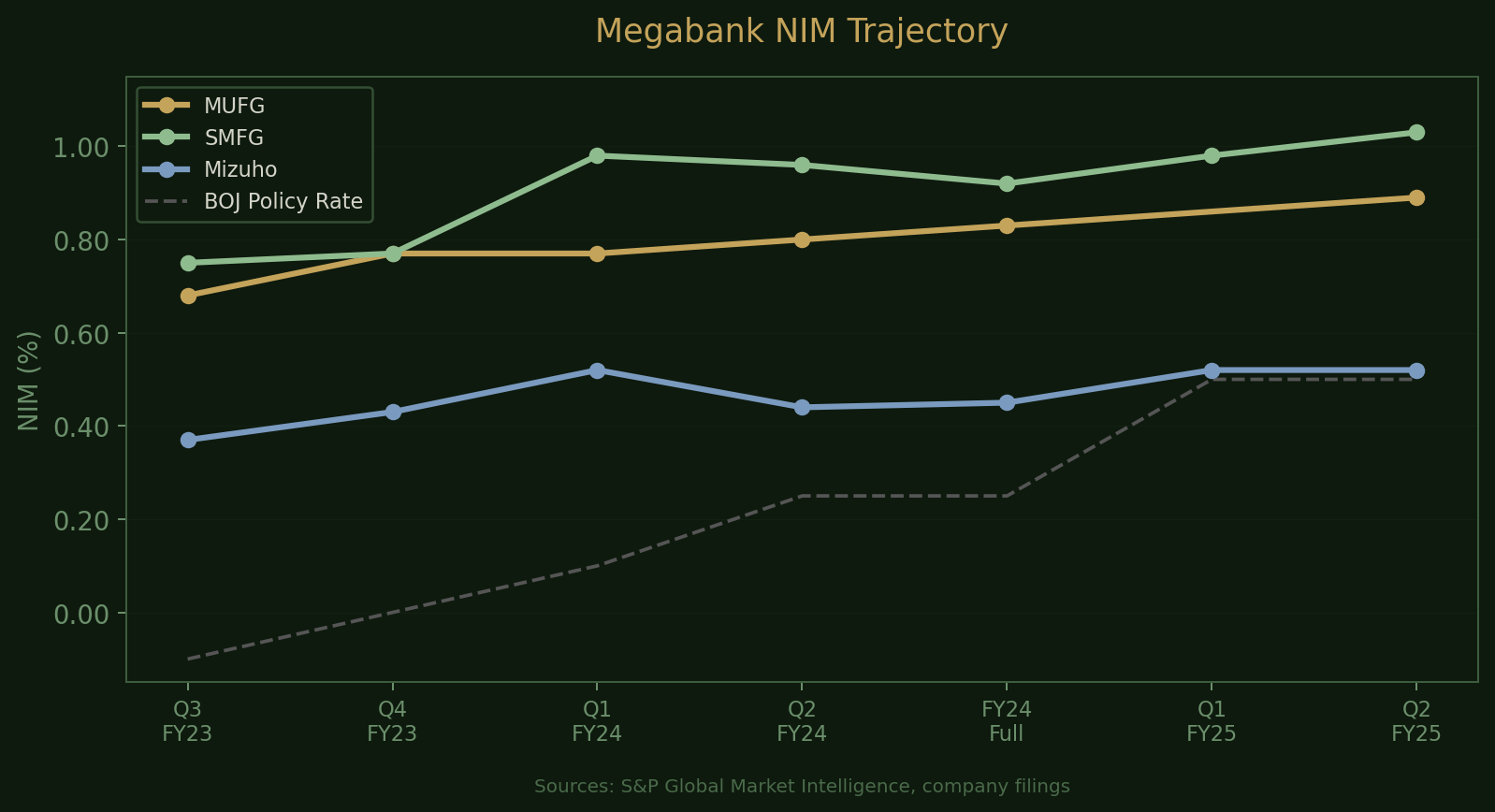

The trajectory makes this concrete. MUFG’s net interest margin went from 0.68% in late 2023 to 0.89% by September 2025. SMFG’s rose from 0.75% to 1.03%. Mizuho’s domestic loan-deposit spread climbed from 0.76% to 1.07%. The curve of improvement is steepening, not flattening.

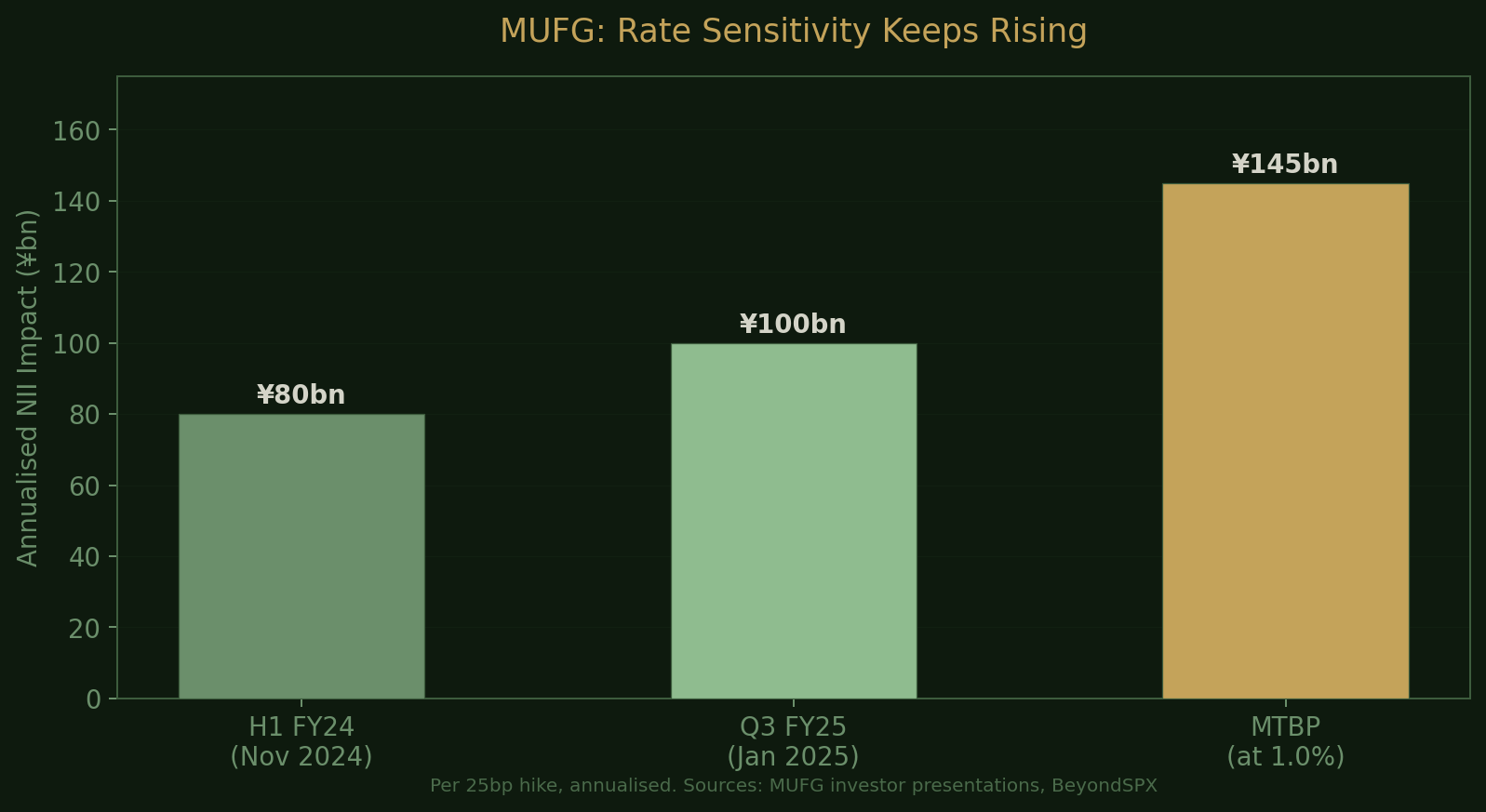

More revealing still is how MUFG’s own sensitivity estimates have evolved. In November 2024, the bank reckoned the July rate hike would add 25 billion yen in the current year, 40 billion the next, and 80 billion the year after. By January 2025, the estimate for the latest hike was 20 billion yen now and 100 billion annually thereafter. The medium-term plan pegs the gain at 140-150 billion yen per year at a 1% policy rate. Each time the bank revisits the arithmetic, the answer is larger than before.

Two engines, one curve

The policy rate is only one channel. The shape of the yield curve is the other.

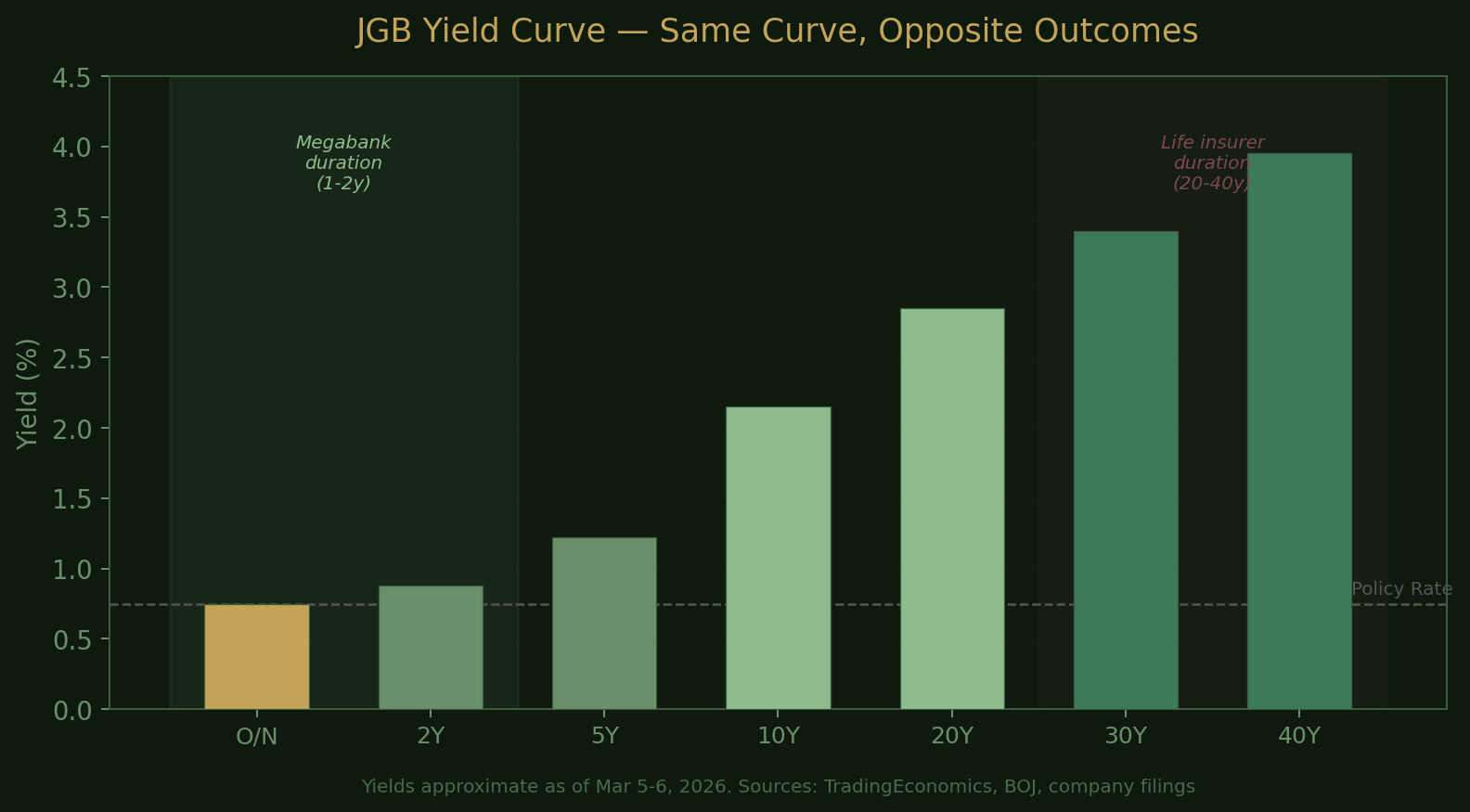

Japan’s government bond curve is the steepest in the G7. Ten-year yields sit at 2.15%, thirty-year at 3.4%, and the forty-year touched 4.24% in January. Between the 0.75% policy rate and the long end lies roughly 265 basis points of spread. Who benefits from this depends entirely on where you sit on it.

Life insurers, for their part, are in pain. They spent the zero-rate era loading up on low-coupon ultra-long JGBs that now carry deep unrealised losses. Japan’s new economic-value solvency regime, J-ICS, introduced in April 2025, transmits movements at the 30-to-40-year point directly into balance sheets. Nippon Life, Meiji Yasuda and several mid-tier firms have been scrambling to derisk.

The megabanks occupy the opposite end. Mizuho’s JGB portfolio has an average remaining maturity of 1.8 years. MUFG has shortened its to 1.1 years. At those durations, rising yields are a friend: mark-to-market losses stay small, and maturing bonds roll into substantially higher-yielding paper.

The interesting development is what comes next. In February, MUFG’s CFO office indicated the bank would begin cautiously rebuilding its JGB position as long-term rates appeared to peak. SMFG has signalled much the same. Its investor materials describe an ongoing shift from short-term to medium-and-long-term bonds as representing upside not yet captured in the headline rate-sensitivity figures. If the megabanks start extending duration into a steep curve, the NIM gamma gets a second engine.

The bond-loss red herring

Sceptics point to unrealised losses. MUFG’s hit 200 billion yen at end-December, up from 40 billion at end-March. Regional banks collectively carry around $21.3 billion in paper losses.

Context spoils the narrative somewhat. MUFG sold longer-duration bonds between September and December to limit the damage. The remaining 200 billion is under 10% of a 2.1 trillion yen profit forecast. Held-to-maturity bonds redeem at par. And a portfolio with an average duration of barely a year does not carry much rate risk to begin with.

The regional bank story is different and worth watching. Japan is absurdly overbanked: 62 tier-one regionals, 37 tier-two, and five city banks. Consolidation is finally accelerating, helped by the JFTC’s 2020 decision to lift same-prefecture merger barriers. Daishi Hokuetsu and Gunma Bank plan to integrate; Chiba Bank has taken a stake in its local rival. Funds like Ariake Capital have built positions in more than ten targets. For megabank investors, though, the conflation of regional distress with megabank fundamentals is less a risk than an opportunity: the same headlines that suppress valuations do not apply to banks earning 2 trillion yen a year.

Shareholders get paid

The capital-return story reinforces the point. MUFG has authorised 500 billion yen in buybacks for fiscal 2025, its largest ever. Mizuho is buying back 300 billion, its first programme in 16 years. SMFG added 150 billion. Together, 950 billion yen in repurchases alone.

The unwinding of cross-shareholdings provides a further tailwind. SMFG booked 196 billion yen in gains from equity disposals in the first half. These are not one-off windfalls. The Tokyo Stock Exchange’s governance reforms demand ongoing reductions, and the banks still hold large portfolios of legacy stakes. This is a multi-year earnings stream.

A curious asymmetry

Foreign investors have been net buyers of Japanese equities for ten consecutive weeks. The latest weekly inflow was 973.9 billion yen, double the prior week. CME Micro Nikkei futures volume is up 60% month-on-month.

Meanwhile, Japanese retail investors continue to channel their savings into eMAXIS Slim All Country, an index that holds no megabank in its top positions. Every month, Japanese savers fund overseas equity markets while foreign institutions accumulate the very financials those savers overlook. Whether this constitutes a mispricing or merely a difference of opinion is a question the next few years will settle.

The NIM gamma does not require aggressive tightening. A gentle path to 1%, which swap markets price at roughly 65% probability for an April move, is sufficient. The convexity is already embedded. Each hike reveals a little more of it.

This article reflects my own reading of publicly available information and is not investment advice.